Smarter Loans Inc. is not a lender. Smarter.loans is an independent comparison website that provides information on lending and financial companies in Canada. We work hard to give you the information you need to make smarter decisions about a financial company or product that you might be considering. We may receive compensation from companies that we work with for placement of their products or services on our site. While compensation arrangements may affect the order, position or placement of products & companies listed on our website, it does not influence our evaluation of those products. Please do not interpret the order in which products appear on Smarter Loans as an endorsement or recommendation from us. Our website does not feature every loan provider or financial product available in Canada. We try our best to bring you up-to-date, educational information to help you decide the best solution for your individual situation. The information and tools that we provide are free to you and should merely be used as guidance. You should always review the terms, fees, and conditions for any loan or financial product that you are considering.

Getting a business loan in Calgary can be a long and tedious process. Although banks and credit unions in the area offer business loans, these traditional institutions tend to move slowly, and have strict requirements for business loan approval. So unless you meet very specific criteria and have a lot of time to spare, they can’t do much for your business.

Fortunately, because the online financial market has grown so significantly in the past few years, there are a number of online business loans now available to Calgary businesses, from reputable alternative lenders. These lenders offer flexible terms and competitive interest rates, making them a good business loan option even for those who might be approved to borrow from their local bank. No matter what you need money for – to purchase equipment, to expand, for real estate, operating expenses, or any other reason – online lenders have the business financing you need to succeed.

At Smarter Loans, we have researched the marketplace to find you the best business loan providers in Calgary, and you can see all their offerings and requirements before applying online. Just take a look at the table below to find the right loan and lender for you. It’s then a matter of a few simple clicks to fill in an online application form to get your business the help it needs.

You can also pre apply with us, and let us connect you with the best business loan provider for your circumstances in Calgary.

And for more on business loans, how they work, business credit scores, and other sources of business funding, read the page below.

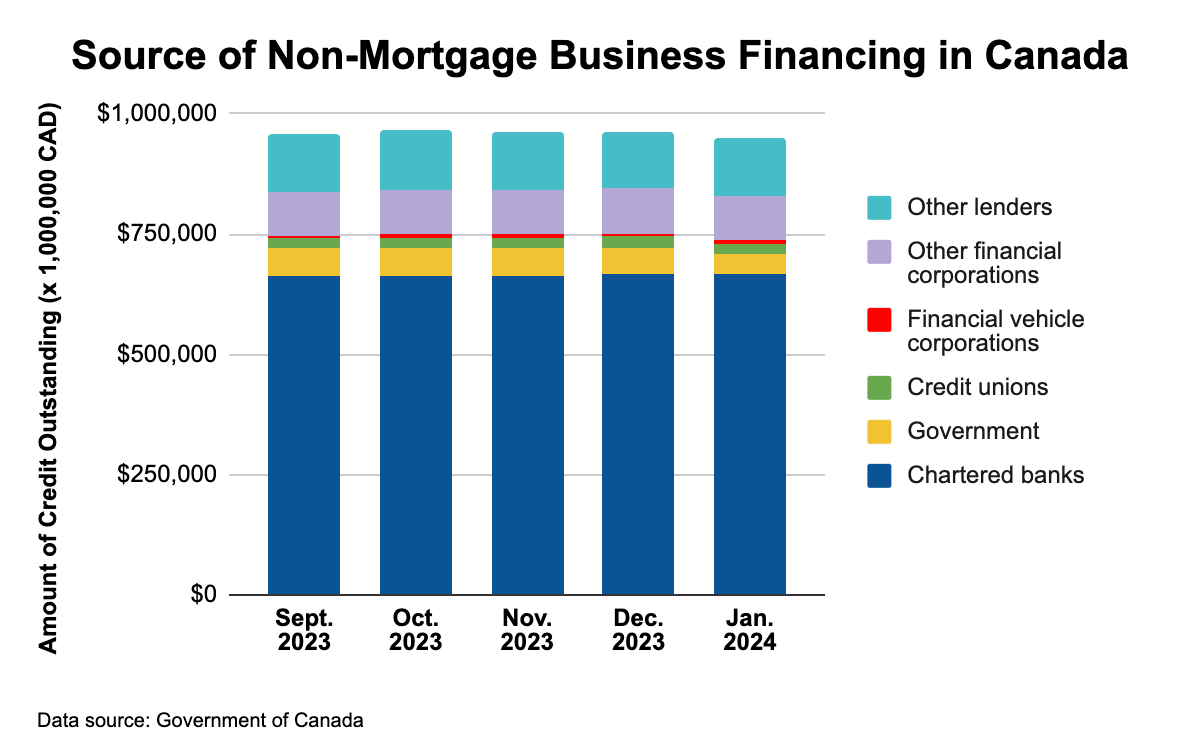

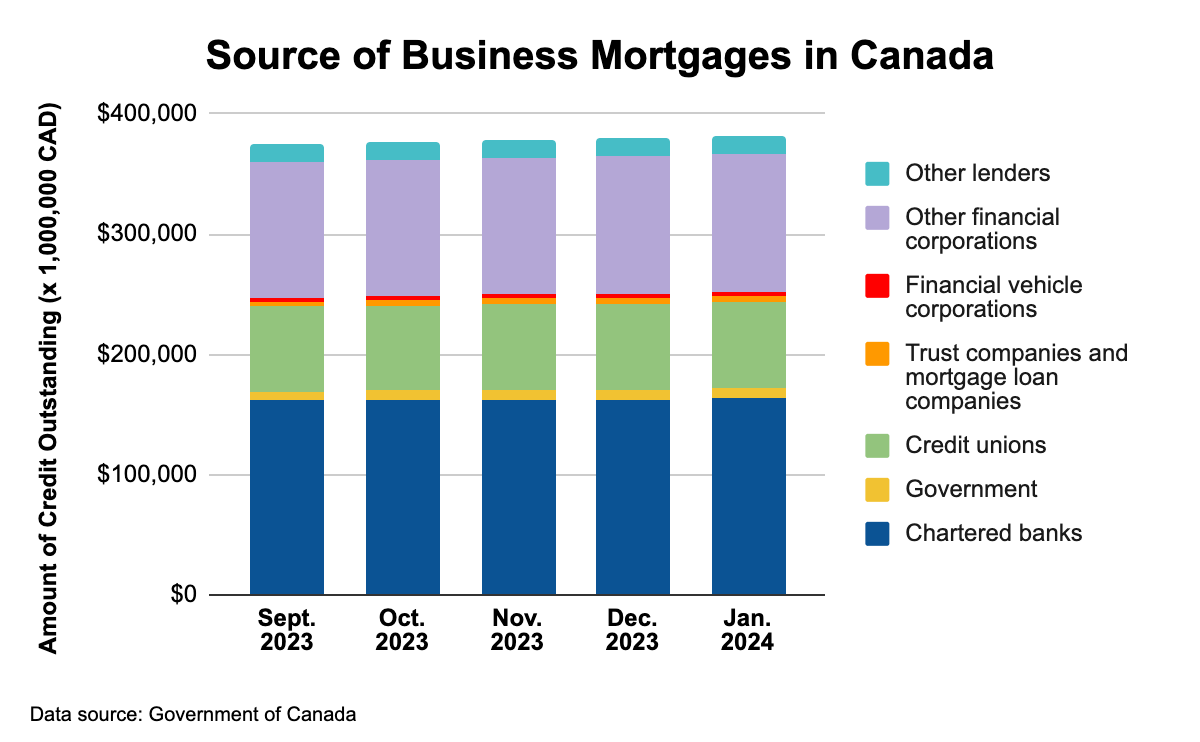

There are three major types of lender for Calgary business loans:

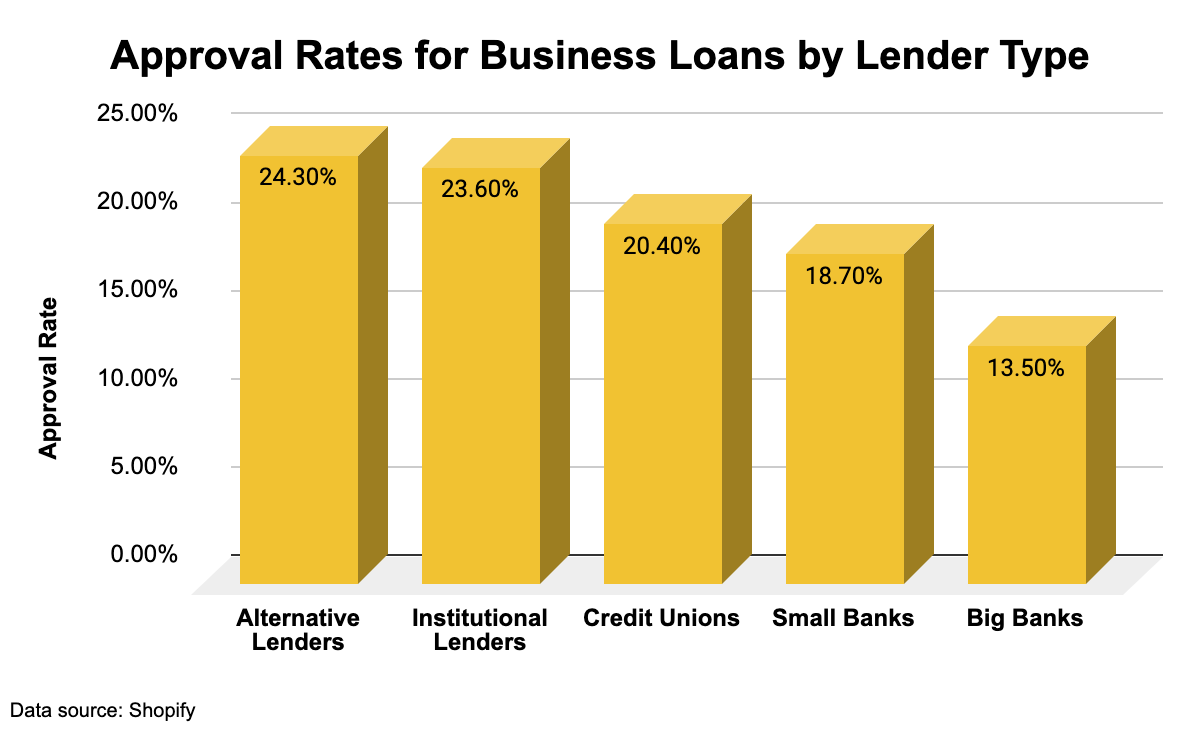

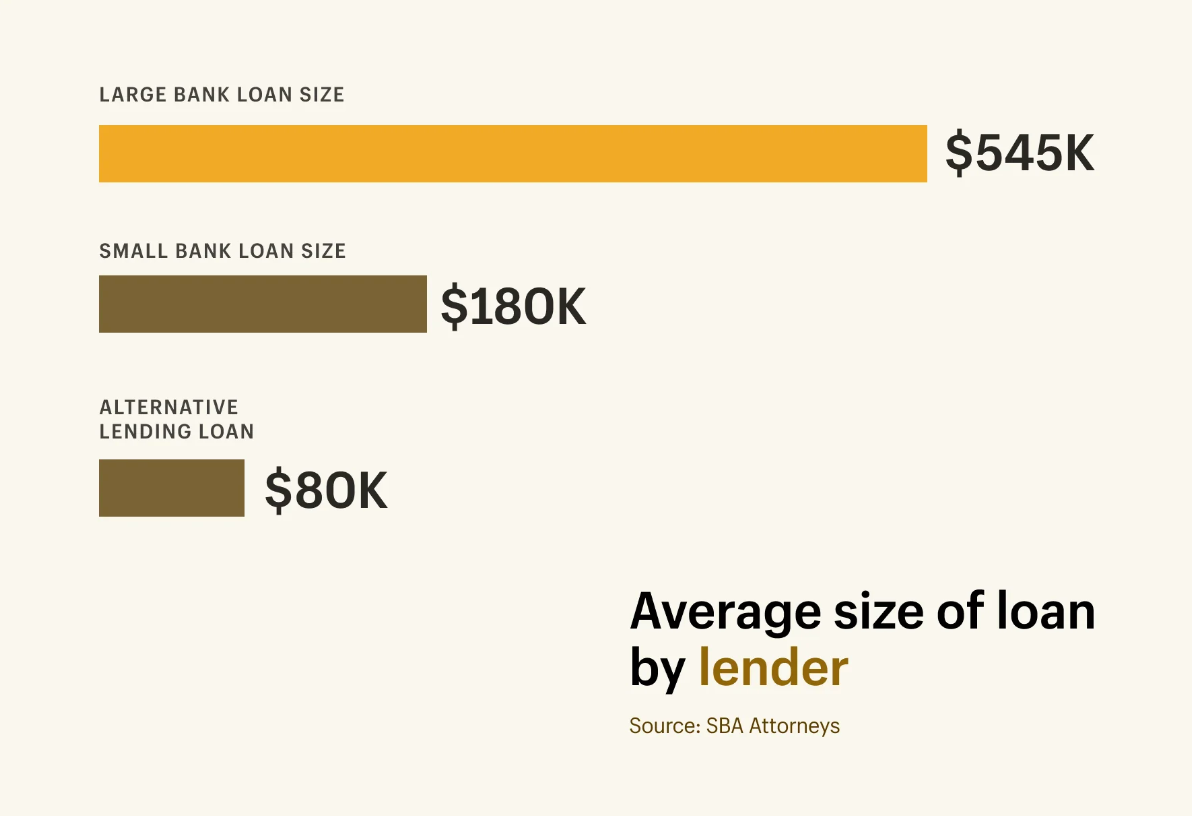

Banks and Credit Unions

Banks and credit unions offer various types of business financing and other services, including term loans, lines of credit, and business credit cards. Business loans from a bank might offer good rates, but often come with strict eligibility criteria (usually related to age of the business and financials), and can take a few weeks for funding to come through. If you have an existing business bank account though, they might be able to fund you.

Government

Another option for funding your business is to see if your business qualifies for a government loan program, like the Canadian Small Business Financing Program. This program does not mean the government itself is offering loans; rather, it helps other lenders, such as your bank, provide loans to those it might not otherwise be able to, by sharing the risk with them.

Both term loans and lines of credit are available, and most small businesses in Canada are eligible for funding, for a variety of purposes, including equipment purchase, existing leasehold improvements, moving from leased property to purchasing property, securing intangible assets, to cover working expenses, and so on.

For more information on the Canada Small Business Financing Program, see here. And to find out about all the business benefits offered by the government, see here.

Alternative and Online Lenders

Lastly, there are alternative lenders. This group encompasses many different types of companies, many of which are wholly online. Lenders in this category accept a wide range of applicants, and usually have more flexible terms and faster processes than traditional financial institutions. This means that if you have bad credit, a brand new business, are self-employed, or simply want to avoid the hassle of going to your bank, you should be interested in an alternative lender. It’s also worth noting that some equipment vendors offer financing, and they fall in this category too. And business credit cards are available from digital providers as well as your bank.

Every lender requires that their borrower meets specific criteria for a business loan, and these criteria can vary by lender type and by individual company. At the most basic level, your business will need to be:

Past these very simple requirements, you will have to provide the following paperwork to demonstrate your business’s viability and justify the loan application:

There are some lenders who only offer loans to specific industries. Be sure you meet the requirements of the lender you want to secure a loan from, before you apply.

When it comes to securing business loans in Calgary, understanding the nuances of interest and other costs is crucial. This knowledge ensures that you’re choosing the right type of financing for your needs.

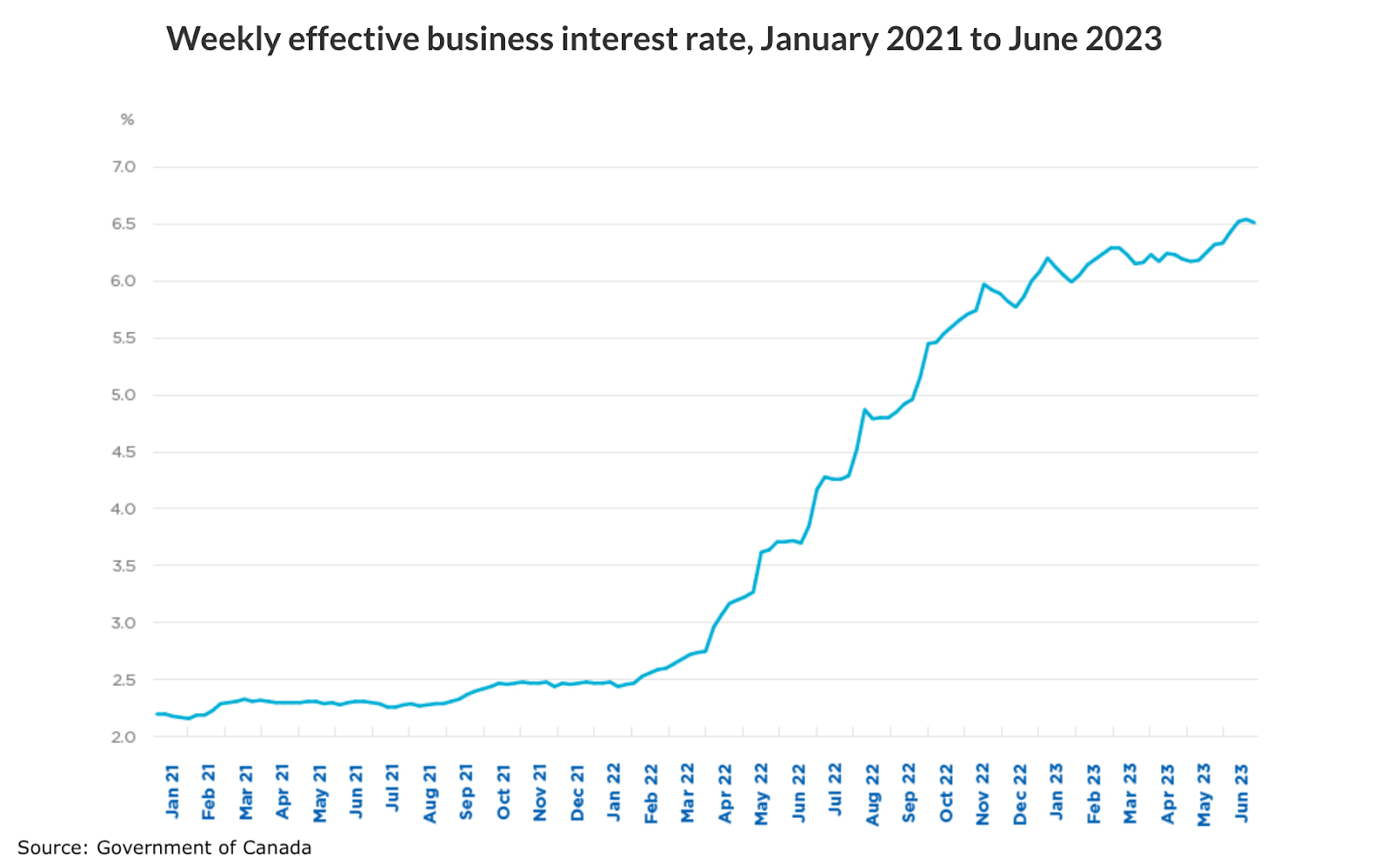

Calgary business loans and business credit cards typically come with two types of interest rate: fixed and variable. A fixed interest rate means repayment stays steady, providing stability and predictability. A variable interest rate can fluctuate, meaning your repayments can increase or decrease. To understand regulation around how much interest can be charged, see here.

Your credit score plays a significant role in determining the interest rate you’re eligible for. A high score can secure lower interest rates and better loan terms, whereas a bad credit score might lead to a higher interest rate or require you to seek financing from a dedicated bad credit lender.

Business loans in Alberta come with various additional costs, such as origination fees, application fees, and late payment penalties. Understanding these fees is essential for calculating the true cost of your loan over its whole life.

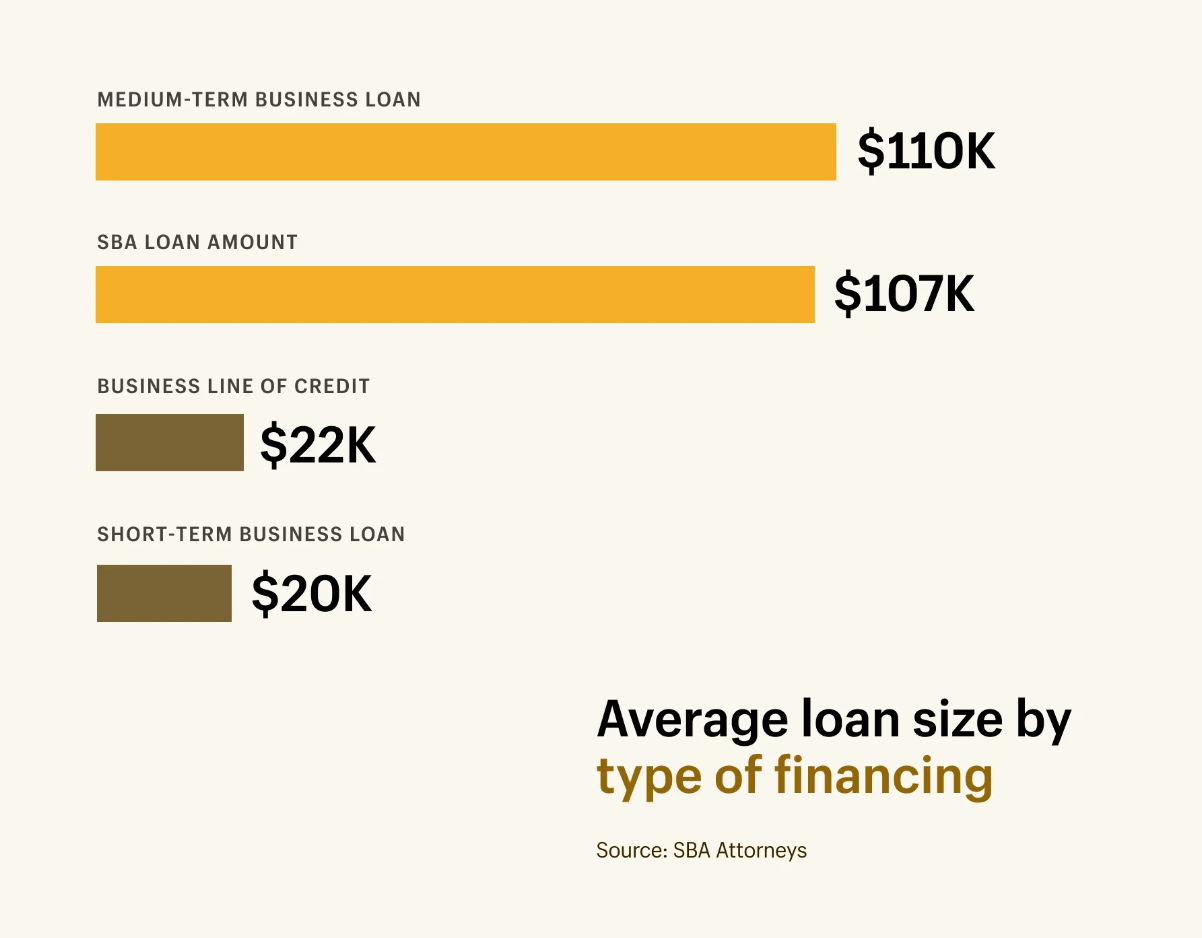

The loan amount you request should align with your business’s financing needs and your ability to repay. Larger loans provide more capital, but also come with higher repayment obligations. It’s crucial to assess how the loan supports your business’s growth or working capital needs without adversely affecting your cash flow.

When securing a business loan in Calgary, one of the first things a lender will look at is your credit score. Institutions use this score to assess the risk of lending to you, and it will directly impact whether you are approved to borrow. In addition, a high score can open the door to lower interest rates, larger loan amounts, and better financing terms. A lower score might limit your options, leading to higher interest rates or the need for secured loans, where you must obtain the loan with collateral like equipment or other assets.

Understanding credit – both business and personal – can be a game changer for entrepreneurs looking to finance the growth of their business.

Improving your credit score doesn’t happen overnight, but with the right approach, you can enhance your appeal to lenders. Here’s how:

Gathering the paperwork needed for a business loan application can feel like a daunting task, especially when you’re eager to secure funding and focus on the growth of your business. But preparing the documents for your application properly can save you significant time and make it easier to secure the money you need. So let’s take a closer look at them:

A comprehensive business plan is your first step towards loan approval. This document outlines your business model, market analysis, operational strategy, and competitive analysis. It’s not just a formality; it’s a chance to convince others of your company’s potential for success. Your business plan is also where you can outline the intended use of your loan funds.

Financial projections are also critical. Lenders want to see your expected revenue and expenses over the next few years. This demonstrates your ability to pay back the loan. Include profit and loss statements, cash flow forecasts, and balance sheets. Realistic projections can significantly increase your chances of securing business financing.

Lenders in Canada often require personal financial information to assess your reliability as a borrower. This may include personal tax returns, a personal net worth statement, and details of assets and liabilities.

Your application must also include up-to-date business financial statements. These documents provide a snapshot of your company’s financial health; be as thorough as you can. Up-to-date accounts as well as past tax returns are probably necessary.

You also need to show proof of business ownership and any legal documents related to your company, such as incorporation certificates, leases, or franchise agreements. These documents help lending institutions verify your business’s legitimacy and legal standing.

Lastly, if you’re applying for a secured loan to purchase equipment or expand operations, you’ll need to provide details about the collateral. This could be property titles, equipment invoices, or other assets you plan to use as security.

For those with bad credit or unique financing needs, alternative lenders offer Calgary business loans with more flexible terms. These lenders may provide term loans, working capital advances, or business credit cards, each with distinct terms and interest rates designed to assist those in difficult or unusual circumstances.

Alberta business loans have a range of interest rates; lenders base each loan’s rate on factors like your credit score, the type of financing, the business’s cash flow, and so on. Generally, rates can range from as low as 3%, to over 20%. It’s essential to shop around and compare offers to secure the best rate for your business.

Many banks and financial institutions in Canada offer online applications for business loans, making it convenient to apply. However, some situations might require a personal meeting, especially for larger loan amounts or complex financing arrangements.

Online lenders rely solely on digital communication; they will use the loan application stage to gather all the information they need. Just bear in mind that some online providers have limited customer service capabilities, so choose one that can provide the finance you need and the service you require to manage your loan account.

A secured business loan requires you to provide collateral (like equipment or real estate) that the lender can seize if you fail to repay the loan. An unsecured loan does not require collateral but often comes with higher rates due to the increased risk to the lender.

To find out if you qualify for government grants or incentives in Alberta, visit official government websites or contact local business support services. These resources can provide detailed information on eligibility criteria for various programs aimed at fostering business advancement and innovation.

If your business loan application is rejected, ask the lender why. This feedback can help you address any issues, such as improving your credit or adjusting your business plan.

Yes, Calgary and the wider Alberta region offer several financing options tailored for startups, including government-backed loans, venture capital funds, and business incubator programs. These funding sources are designed to support the unique needs of entrepreneurs looking to launch and expand their companies.

These companies are recognized for their excellent service, product offering and financial literacy education for all Canadians.