As an investor, I always had the best intentions on my mind when it came to long-term investing. It was pretty clear to me; start investing early, choose the right assets, and stay invested. You would be surprised to know that I opened my first bank account in the third grade.

Unlike most of childhood habits or dreams, I didn’t outgrow saving or investing. (Turns out it was a much better personal choice than becoming a ballerina)!

My first definitive investing step: A TFSA

Fast forward to graduation and getting my first corporate job, I took one of many definitive steps towards long-term savings, which was to open a TFSA account. TFSA or Tax Free Savings Account is one of the most efficient investment options for individuals, allowing you to invest in pretty much any asset class, such as:

- stocks

- bonds

- ETFs

- guaranteed investment certificates

The primary reason why I opened it is because of a piece of advice from a random banker. Going by its benefits, tax-free withdrawals, and investment options, it made perfect sense only until I realized that I was making a terrible mistake.

Once I got a committed financial advisor, one of the first things she noticed was that I was investing through a high risk TFSA, not suitable for a graduate, thereby helping me realize a critical aspect of investing. You need proper financial awareness, knowledge for DIY investing success.

Wealthsimple: Getting started with the robo advisor

Despite being someone looking out for excellent, economically viable financial advice, choosing a robo advisor wasn’t an easy decision. Having an algorithm decide my financial fate was too much of an ask, but then I decided to keep my prejudice aside and use logic, not emotion, to arrive at the final decision.

What I like about Wealthsimple

Takes 5 minutes to get started: Unlike a traditional financial management consultation, you need only 5 minutes to signup for Wealthsimple. You begin by answering questions about your financial goals, choose a risk level, and link your account to make a deposit. That’s it!

Choose between different risk levels: Since I am decades away from retirement, I can be aggressive with my investments, and I like the fact that Wealthsimple allows me to define my risk profile. You can select among conservative, moderate-risk, and aggressive investment portfolios.

Affordable management fee as your account grows: If you’re anything like me, you probably pay special attention to the management fees. Wealthsimple starts you in the 0.5% management fee tier until you cross $100k mark, and post that, the fee drops to 0.4%. What’s even better is that you get exclusive features in the second-tier such as financial planning sessions, tax-loss harvesting, tax-efficient funds, and other perks.

Smart features such as roundup: To be honest, making a contribution every month could be daunting, especially if you’re new to the financially disciplined life. Wealthsimple offers features such as automatic roundup, which allows you to contribute a little with every financial transaction. If your weekly shopping bill was for $407.20, Wealthsimple will round it off to $408, and contribute $0.80 towards your account automatically.

Invest using the right investment account: One of the common mistakes people make is choosing the wrong investment account as I did. Wealthsimple picks the correct investment account for you. The options include TFSA, RRSP, RESP, RRIF, LIRA, and other regular savings, investing accounts.

Socially responsible investing option: Another thing that caught my eye was the option to choose socially responsible investments. Wealthsimple provides multiple options, such as investing in low carbon stocks, stocks with a positive human rights record, pro-environment companies, cleantech stocks, and government securities.

High-interest savings account: Having a high-interest savings account along with all the investment flexibility Wealthsimple offers was the cherry on top for me. Getting a flat 2% interest rate for all of my savings without any account minimums, unlimited free transactions, and nil balance fee had me hooked for good.

Ability to trade, and tax-loss harvesting: I realized it later only that Wealthsimple has a trading module and offers zero-commission trading to their account holders. Additionally, they provide tax-loss harvesting, which could help in lowering your net taxable income.

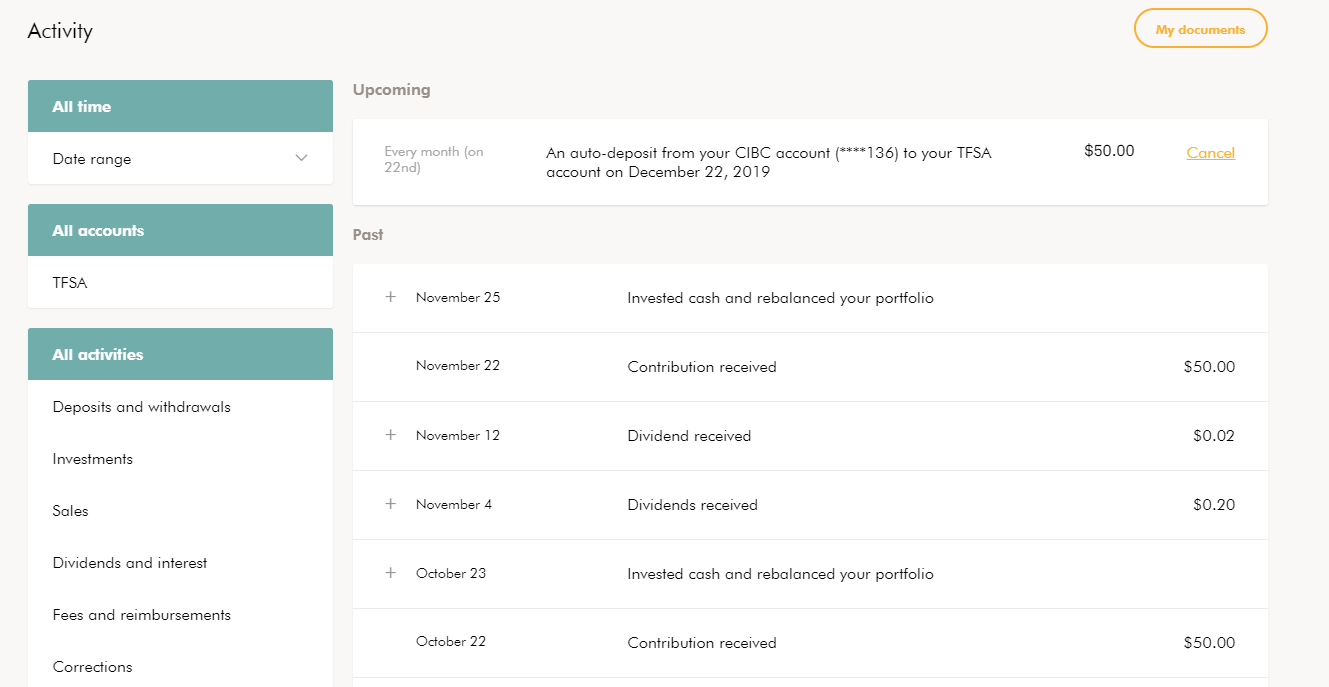

Here is how I have invested so far

Using auto-deposits

The easiest way to invest without falling behind is through auto-debits, and I am using this feature as well. You can see how Wealthsimple credits dividends and reinvests it, along with automatic rebalancing of my portfolio. Here is how it looks:

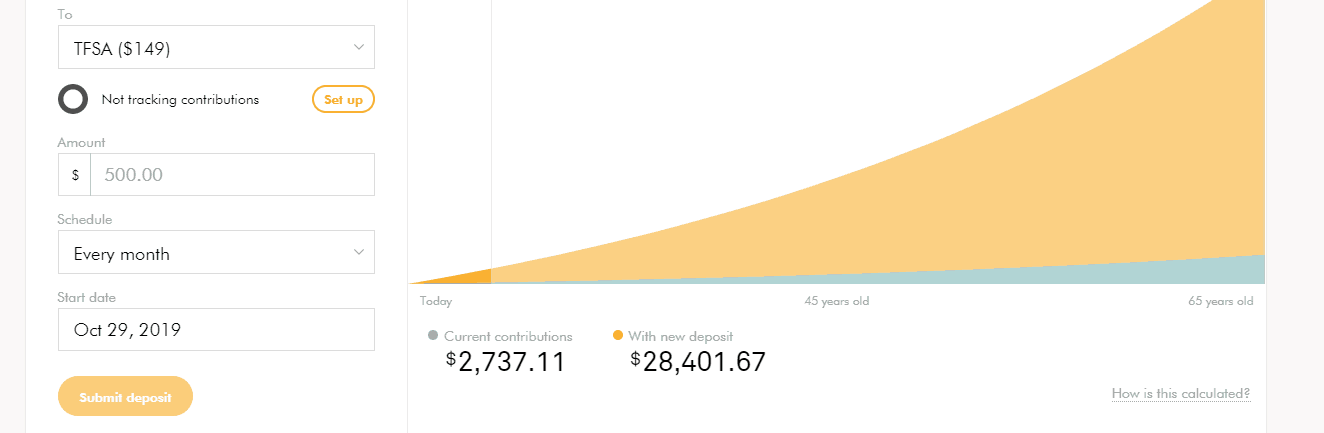

My investing/returns prediction

While I have just started investing, it’s always good to look at the graphical prediction of the returns, being able to save all that money is an amazing feeling.

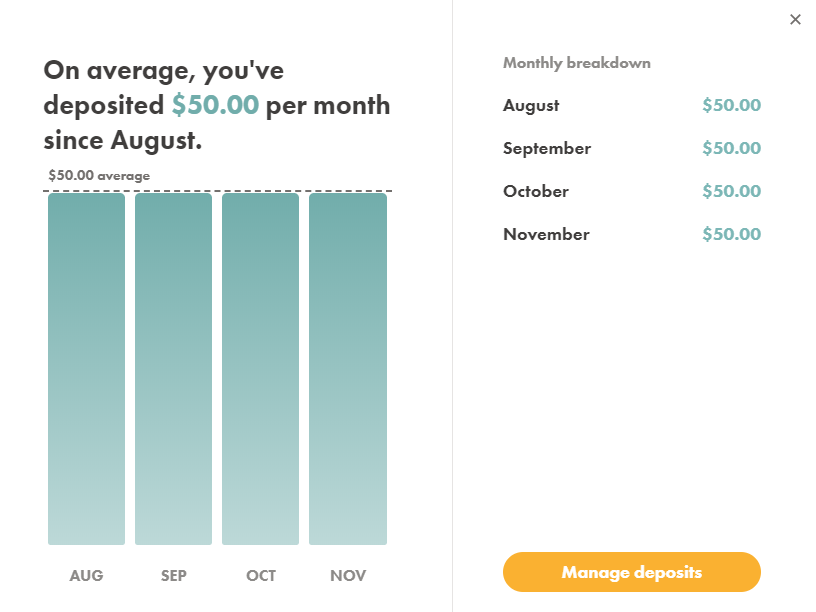

Going steady with investments

I aim to save consistently with the auto-debit feature, roundup feature. In addition to offering excellent investments, Wealthsimple scores high for the ease of investing, having an intuitive user interface, and giving access to financial planners whenever you want.

Wealthsimple: A financial advisor for every investor (Beginner, Intermediate, or Pro)

If I am to rank the number one feature of Wealthsimple for investors, it would be the versatility of its investment service. As an intermediate investor, I have every tool, asset class, or service that I’d require for my investments over several years. The same is applicable for both beginner as well as pro investors.

If you’re just starting with your investments, Wealthsimple guides you through the entire process. Similarly, if you are an experienced investor, Wealthsimple gives you multiple diversification options, along with the ability to set custom portfolios. If you need to contact support or require specific services, just reach out to their financial planners at the tap of a button.

![]() Written by:

Written by:

Jenna West is Smarter Loans' in-house financial writer and content director. She has been covering the Canadian FinTech and finance industry since 2017, including financial trends analysis, industry surveys, regulatory updates and changes in Canadian consumer behaviour when it comes to finance.