Compare Lenders

Discover Popular Financial Services

What is the Mid-Market?

There are a few different ways to define mid-sized firms. The primary two are:

- Companies that employ 100-499 people

- Companies with annual revenues between $10 million and $1 billion

Clearly, the above criteria define a wide range of businesses, and the statistics bear this out:

- In Canada and the U.S., there are over 200,000 companies that count as mid-market

- Mid-market firms account for over 30 million jobs in North America alone

- 16% of Canadian jobs are for mid-market businesses

- Canadian mid-market companies contribute 12% to the country’s GDP

- The average revenue for Canadian mid-market firms is $34 million

Financing Challenges in the Mid-Market

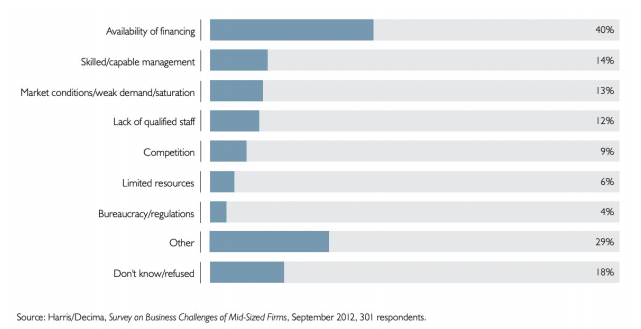

Interestingly, despite the number and breadth of mid-market companies and the industries they represent, their numbers are dwindling. Studies show that on average, 14% of Canadian mid-sized firms shrink to small business levels, or close entirely, each year. One of the problems many mid-sized firms face is a lack of available financing to maintain operations or to expand to meet their competition. 40% of surveyed business leaders in this market cited this as their primary barrier to growth, despite the fact that 65% of mid-sized firms need financing on a three-year cycle.

Barriers to Growth for Mid-Sized Canadian Companies

Many businesses automatically think of standard business loans when considering financing, but this is not always an option for mid-sized companies. These companies are too large for small business loans and their attractive, often government-mandated terms, but too small to qualify for large bank loans and the economies of scale that benefit large corporations. So it’s hard to raise capital, and the cost of debt is higher for mid-sized companies. They sit in an awkward middle space, which luckily has been filled by a diverse set of lenders able and willing to work with mid-sized companies.

Mid-Market Financing to the Rescue

The gap in mid-market financing has been filled by all kinds of traditional and non-traditional lenders, and the number of these mid-market lenders has rapidly increased over the past few years. Mid-market loans are typically in the range of $2 million to $100 million, and can be used for many different purposes, in many different industries.

Industries that might rely more heavily on these types of financing include:

- Manufacturing

- Trade

- Forestry

- Agriculture, fishing and hunting

- Construction

- Mining and natural resources

- Trucking and transportation

- Marine and aviation

- Professional services

- Social services

Types of Mid-Market Loans

The number of lenders now working in this middle space has increased, and so have the types of loan available to mid-sized companies. Given the borrowers in this field have different challenges and needs compared to their smaller and larger brethren, these alternative types of loan can be better suited to mid-sized companies than traditional bank loans. But what are these alternatives?

Bridge Loans

A bridge loan is a short term loan, often backed by company collateral (such as property or inventory), and typically used to expand operations or to assist with cash flow. Loan duration ranges from a few months to three years, as bridge loans are intended to be in place only until the company secures more permanent financing, or removes an existing obligation. Essentially, they help with short term cash flow, and so come with high interest rates and more punitive terms than longer term loans.

Asset-Based Loans

An asset-based loan is what it sounds like: a loan secured against some asset(s) of the borrower. These loans are used when a company needs to raise capital for operations or growth, but cannot get a traditional loan from a bank; the securing asset can be anything, from property, to inventory, to equipment, to accounts receivable. What is considered an eligible “securing†asset will vary from lender to lender, but it cannot be used as collateral on another loan or be at risk from legal proceedings or tax issues.

Asset-based loans are often used like revolving lines of credit, to continually raise working capital to cover expenses or investments. Their interest rates and other loan terms vary. A typical APR ranges from 7% to 17%.

Inventory Finance

Inventory financing is financing used to purchase new inventory or to leverage the value of existing inventory. This is especially helpful when large amounts of inventory are needed quickly, or when company assets are tied up in inventory and cash flow is becoming a problem. With this type of loan, it is important to ensure that you have a reliable inventory tracking system and perpetual inventory.

Direct retail companies cannot qualify for these loans; instead they are designed for manufacturers, wholesalers and distributors that need a minimum of $500,000 in ongoing financing. These loans are easier to get than bank loans, and the loan amount can grow as sales grow.

Accounts Receivable Financing

If you have customers or other businesses with outstanding invoices, and are struggling to find a loan, then accounts receivable financing might be for you. This type of loan is based on the amount owed to you by others, and can be structured in a few different ways, usually with the lender accepting the risk of uncertain payment timelines from the accounts receivable. In essence it’s like a swap: short term financing in lieu of longer term cash flows.

Qualifying for this type of financing can be tricky, as although accounts receivable are considered liquid assets, they are not always easy to collect. Depending on your company’s circumstances, they can also be more expensive than traditional loans. They do however allow companies to get access to quick cash, and remove the worry of account collections.

Heavy Equipment Financing

Heavy equipment loans are designed for one purpose: the purchase of new heavy-duty equipment, such as production line machinery, specialized technology, and commercial vehicles. These items can be very expensive but necessary to continue operations or to expand.

Heavy equipment loans are available from a variety of lenders, including traditional banks, and rely on the machinery itself as collateral. Loans usually range from $5,000 to $500,000, and as with many other loans, the most competitive interest rates are reserved for companies in the best financial position. Most lenders require a minimum of two years of business history and a minimum credit score to qualify.

Capital Lease

A capital lease is a useful way to get access to an asset you might otherwise not be able to afford. The way it works is that the borrower (or lessee) gets to use the asset (equipment, property, etc.) as if they own it, and are responsible for all of the ongoing maintenance costs associated with the asset (for example, insurance, repairs, taxes). But the asset is actually owned and funded by the lender.

These are fixed-term agreements that cannot be renegotiated; at the end of the lease, the borrower has the option of purchasing the asset for a reduced sum. This structure allows businesses to access needed assets quickly, and remain flexible in their business operations should other needs arise. There are also some tax benefits to capital leases because of the way they are structured.

Sale and Lease Back

A sale and lease back (also known as a leaseback) is a simple transaction where a company sells an asset for the income, and then leases the item back. So in effect, you no longer own the asset, but you still get to use it. These are typically long-term agreements based on fixed assets, like real estate. They are useful if a company has high cost fixed assets but are cash poor, and need the capital invested in the asset for operations - but also still need to keep using the asset.

TRAC or Split TRAC Lease

TRAC stands for Terminal Rental Adjustment Clause, and a TRAC lease is used for the lease of vehicles and trailers. These agreements are based on the borrower and lender pre-agreeing (before the lease starts) to an estimated residual value of the vehicle at the end of the lease; once the lease has expired, the borrower must pay this amount to secure the final purchase of the vehicle. It’s beneficial in that both the lender and borrower know the payment schedule and final purchase amount in advance; the borrower gets access to needed equipment, and the lender has guaranteed lease payments and final payout. A split-TRAC lease is very similar, but the borrower’s exposure at the end of the lease term is limited.

Tax and Non-Tax Leases

“Tax lease†refers to any lease where, for tax purposes, the lender remains the owner of the leased asset. Here’s an example: a capital lease (discussed above) relies on the asset being transferred to the borrower’s ledger, essentially meaning that for tax and accounting purposes, the asset becomes the borrower’s. This is a non-tax lease. But in an equipment lease, where your business pays a monthly sum for the use of some equipment, the ownership of that equipment remains in the hands of the lender. So for tax purposes, the costs and benefits of ownership do not change. This is a tax lease.

The advantages and disadvantages of tax and non-tax leases depend on your particular circumstances and your company’s accounting and tax needs. It’s always important to take these factors into consideration when choosing a loan or lease of any kind, as they can be significant.

There is clearly a plethora of financing options available for mid-sized companies, with many engineered to address industry-specific issues that traditional lenders ignore. Whatever your industry or your company’s financial situation, always do your research before committing to financing. You might well find more competitive terms or better options through one of the above options.

Frequently Asked Questions About Mid-Market Financing

What is a mid-market company?

A mid-market company is any company that employs between 100 and 499 people, or that has annual revenues between $10 million and $1 billion.

What is mid-market financing?

Mid-market financing is a general term for financing that is available to mid-market companies; this can include traditional loans from traditional lenders, but also includes other types of loans from specialized lenders.

Why do mid-sized companies struggle to find financing?

Mid-sized companies do not qualify for the attractive loans that are available for small businesses, or the larger loans that are available to large corporations. In Canada, most small business loans are regulated by the government and deliberately made more accessible to encourage small business growth. And larger companies have access to economies of scale and attractive rates from big lenders. But mid-sized companies are stuck in the middle, often failing to qualify for traditional loans.

What are the roadblocks to mid-market financing?

If a mid-sized company can overcome the hurdle of finding a lender to work with, there are still other issues to consider. Most traditional loans are not designed with mid-sized companies in mind, and so can be (relatively) more expensive, involve lengthy paperwork and processing times, and be inflexible to the quick changes mid-sized companies need to adapt to. These factors can sometimes make traditional loans almost useless in comparison to more flexible or targeted loan types.

What industries are mid-market companies in?

Mid-market companies span industries, and can be found across the country. A significant portion are in service-oriented business, such as manufacturing, trade, construction, and transportation.

What kind of financing can mid-market companies get?

Mid-market loans are typically in the range of $2 million to $100 million, and can be used for many different purposes, though they are most commonly used for equipment purchase, upgrade or repair, inventory needs, or to assist with cash flow. There are plenty of lenders who offer mid-market financing to mid-sized companies, with some even providing equipment, transport or inventory specific loans to help you best address your needs.

Amy Orr

Amy Orr is a professional writer and editor with over 10 years of experience in the Canadian, U.S. and U.K. financial markets. She has written for numerous publications on topics as diverse as economic literacy, corporate finance, and technical analysis of numerical data. Prior to transitioning to full-time writing, she worked in the hedge fund sector. Her academic background is astrophysics, and she has a Masters in Finance from the University of Edinburgh Business School.

Jenna West

Jenna West is Smarter Loans' in-house financial writer and content director. She has been covering the Canadian FinTech and finance industry since 2017, including financial trends analysis, industry surveys, regulatory updates and changes in Canadian consumer behaviour when it comes to finance.

Explore more

Similar products

I’m very honoured to shear my experience with this illustrious platform. To be able to systematically choose from a list optional to one’s profile without doing much leg work is truly rewarding. This platform allowed to expand my options and chose which lenders fit my profile, thank you and continue doing what you do best,, connecting people to available wealth opportunities.

When you feel in need of a loan do it smart and make it a Smarter Loans.

Very Helpful, was assisted in a timely fashion and was ultimately able to receive assistance; I highly recommend!!!

I have recommended this place to many friends I feel that this company goes out of their way to help people that they can and they are very easy to work with

This company is reliable, quick, and just has the best customer service and rates it is a easy process with quick results. Would definitely recommend to anyone that needs the help.

Personally love this opportunity and app. Super convenient and easy to use and super awesome variety of great loans. Thanks so much guys for making such an awesome site and app and being there for me over the years. :)

From beginning to end, my experience was great! Very professional and personable agents. They only asked questions that were needed for the loan and payments were extremely reasonable. Would recommend to anyone who needs emergency funds.

“ Thank you SO very much! My situation was tricky and you guys made the whole process so effortless. The way you guys handle the whole process so discreetly. That truly speaks to how well your office is run and the caliber of specialists who handled the processing of my entire loan!”

Why Choose Smarter Loans?

Access to Over 50 Lenders in One Place

Transparency in Rates & Terms

100% Free to Use

Apply Once & Get Multiple Offers

Save Time & Money

Expert Tips and Advice