Best Home Insurance Companies in Manitoba

Pricing varies by product

British Columbia, Alberta, Saskatchewan, Manitoba, and Ontario

Pricing varies by product

All of Canada excluding Quebec

Manitoba Home Insurance Requirements

First things first: who actually needs home insurance? Well, unlike auto insurance, home insurance is not a legal requirement in Manitoba; technically this means that all homeowners and renters can choose not to purchase insurance. However, if you have a mortgage on your home, your mortgage provider will mandate a minimum level of home insurance coverage as a condition of borrowing.

Manitoba Home Insurance Options

There are a couple of different types of property insurance available in Manitoba; although all three are known as “home insuranceâ€, they are actually distinct. They are:

Homeowner’s Insurance

Homeowner’s insurance is what most people think of when they say “home insuranceâ€. This type of insurance covers the physical buildings that constitute a home (including detached structures), personal belongings within the home, and personal liability in the event that someone is injured on the property.

There are different levels of protection within homeowner’s insurance:

- No frills coverage

- Standard coverage

- Broad coverage

- Comprehensive coverage

As well as choosing the level of protection you want for your home via the level of policy you go for, it is also possible to have specific add-ons or endorsements - for example, if you live in a high risk area for a specific peril, such as tornadoes. In general, the more coverage you get, the more your insurance will cost.

Condo Insurance

Winnipeg houses the majority of Manitoba’s condos, and condo insurance is the appropriate form of insurance for residents in these homes. Condo insurance is very like homeowner’s insurance, but it only covers the named unit within a condo building - not the larger building’s structure. The condo building itself will have its own insurance policy to cover the common areas and main structure of the property. Condo insurance is generally cheaper than homeowner’s insurance.

Tenant’s Insurance

Lastly, for the roughly one third of Manitobans who don’t own their own home, there is the option of tenant’s insurance. Tenant’s insurance does not cover the building in question, but it does cover your personal belongings within the building (including items in storage cages in shared areas), as well as personal liability in the event that you cause damage to the building. Tenant’s insurance is the cheapest form of property insurance.

Manitoba Home Insurance Providers

Manitoba is home to over 100 different insurance companies; many of these are national companies, though some are provincial. Manitobans searching for property insurance can go directly to one of these companies for help, or work with an insurance broker to find the best deal. Many insurance brokers and companies have online options to make applying for and purchasing insurance as convenient as possible.

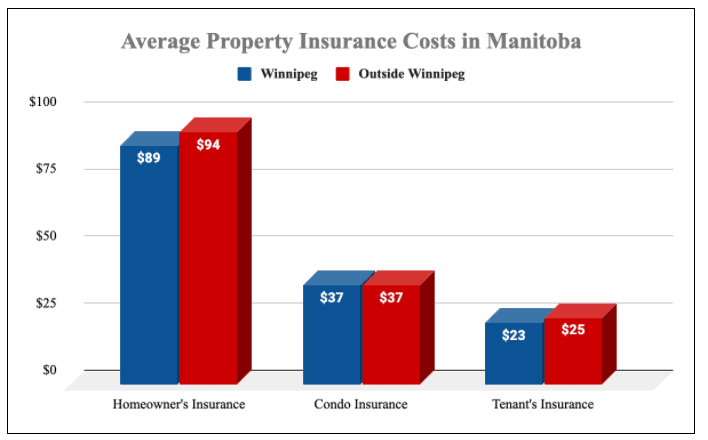

Manitoba Home Insurance Costs

The average homeowner’s insurance policy in Manitoba costs around $90 a month, with condo insurance averaging just under $40 a month, and tenant’s insurance averaging $25. An interesting change in insurance costs happened in Manitoba in July 2020, when most insurance policies became exempt from retail sales tax, saving consumers 7%.

Factors Affecting Insurance Costs

There are a lot of factors that influence the exact cost of a home insurance policy, including:

- Coverage type and level

- Property size

- Property value

- Exact location

- Distance to a fire hydrant

- Age of home

- Condition of home and internal construction type

- Existence of a basement, finished or unfinished

- Type of heating in the home

- Type of plumbing in the home

- Type of wiring in the home

- Type and age of roof

- Presence of smoke alarms, CO monitors and security systems

- Presence of a pool

- Pets in the home

- Number of people resident in the home

- Value of personal belongings in the home

- Presence of high value items e.g. jewellery

- Past claims history

Manitoba-Specific Home Insurance Risks

Manitoba’s location means that it is subject to some fairly varied and potentially devastating weather and environmental events, all of which have an impact on insurance costs. In particular, insurers will be worried about:

- Wildfires

- Tornadoes

- Flooding

- Extreme cold

Most of these events are not covered under standard or basic insurance policies, so be sure to discuss more comprehensive coverage or add-ons with your insurer if you’re in a high risk area.

Frequently Asked Questions About Home Insurance in Manitoba

How can I save on home insurance in Manitoba?

Shopping around is the number one way to save on your home insurance, but you may also try:

- Bundling insurance policies

- Installing a fire alarm or security system

- Paying a higher deductible

- Paying for your policy annually rather than monthly

- Choosing a lower level of coverage

- Asking about discounts

Can I get home insurance for a vacation home?

Yes, absolutely, and protecting your vacation home is important. You can often add vacation property coverage (or mobile home coverage) to your main homeowner’s insurance policy to save money. You can also take out a separate policy.

Who regulates home insurers in Manitoba?

The Insurance Council of Manitoba licenses and oversees insurance companies, agents and brokers in the province. It also regulates and approves rate changes.

Are home insurance premiums tax deductible in Manitoba?

No, unless you run a home business, in which case you will need business insurance coverage as well as your standard homeowner’s coverage. In this case, only the supplemental business insurance will be tax deductible.

Can an Manitoban insurance company deny coverage?

Technically, yes, any individual insurance company can deny you coverage, but this is very rare. If you are denied, you can ask why and potentially solve the problem or find another provider.

Do I need home insurance if I rent my Manitoba property out?

You can use standard homeowner’s insurance if you choose to rent your property out, but you need to be clear with your policy provider about who will be living in the home. And remember that homeowner’s coverage does not cover loss of income from the home, if something happens that prevents you from renting it out. This is why many landlords choose rental property insurance instead.

Written By Smarter Loans Staff

The Smarter Loans Staff is made up of writers, researchers, journalists, business leaders and industry experts who carefully research, analyze and produce Canada's highest quality content when it comes to money matters, on behalf of Smarter Loans. While we cannot possibly name every person involved in the process, we collectively credit them as Smarter Loans Writing Staff. Our work has been featured in the Toronto Star, National Post and many other publications. Today, Smarter Loans is recognized in Canada as the go-to destination for financial education, and was named the "GPS of Fintech Lending" by the Toronto Star.

Discover Popular Financial Services

Why Choose Smarter Loans?

Access to Over 50 Lenders in One Place

Transparency in Rates & Terms

100% Free to Use

Apply Once & Get Multiple Offers

Save Time & Money

Expert Tips and Advice